We care about Aflac’s policyholders affected by the recent wildfires:

To help provide relief for Utah policyholders residing in Utah who were affected by the wildfires, Aflac will provide a premium grace period starting July 31, 2025, and ending Sept. 29, 2025. This grace period also provides an extension of filing deadlines for claims and leniency for any other action required under the policy. Aflac will provide a replacement copy of the policy upon request by the policyholder.

For Network Dental and Vision Members:

This grace period also provides an extension of filing deadlines for claims; relaxation of prior authorization, precertification, and referral requirements; access to appropriate out-of-network providers due to unavailability on in-network providers or the members’ displacement; and leniency for any other action required under the certificate. A replacement copy of the certificate will be provided upon request by the certificate holder. Affected members should contact Aflac Benefit Solutions (formerly Argus Dental and Vision) at 855-819-1873, Option 1, for assistance.

We care about Aflac’s policyholders affected by the recent weather:

To help provide relief for California policyholders residing in Humboldt, Mendocino, Modoc, Napa, Shasta, Sonoma, and Trinity Counties affected by the winter storms, Aflac will provide a premium grace period starting Jan. 31, 2025, and ending Sept. 29, 2025. This grace period also provides an extension of filing deadlines for claims and leniency for any other action required under the policy. Aflac will provide a replacement copy of the policy upon request by the policyholder.

For Network Dental and Vision Members:

This grace period also provides an extension of filing deadlines for claims; relaxation of prior authorization, precertification, and referral requirements; access to appropriate out-of-network providers due to unavailability on in-network providers or the members’ displacement; and leniency for any other action required under the certificate. A replacement copy of the certificate will be provided upon request by the certificate holder. Affected members should contact Aflac Benefit Solutions (formerly Argus Dental and Vision) at 855-819-1873, Option 1, for assistance.

We care about Aflac’s policyholders affected by the recent wildfires:

To help provide relief for Oregon policyholders residing in Oregon who were affected by the wildfires, Aflac will provide a premium grace period starting July 16, 2025, and ending Sept. 15, 2025. This grace period also provides an extension of filing deadlines for claims and leniency for any other action required under the policy. Aflac will provide a replacement copy of the policy upon request by the policyholder.

For Network Dental and Vision Members:

This grace period also provides an extension of filing deadlines for claims; relaxation of prior authorization, precertification, and referral requirements; access to appropriate out-of-network providers due to unavailability on in-network providers or the members’ displacement; and leniency for any other action required under the certificate. A replacement copy of the certificate will be provided upon request by the certificate holder. Affected members should contact Aflac Benefit Solutions (formerly Argus Dental and Vision) at 855-819-1873, Option 1, for assistance.

We care about Aflac’s policyholders affected by the recent wildfires:

To help provide relief for Oregon policyholders residing in Crook County who were affected by the wildfires, Aflac will provide a premium grace period starting July 12, 2025, and ending Sept. 10, 2025. This grace period also provides an extension of filing deadlines for claims and leniency for any other action required under the policy. Aflac will provide a replacement copy of the policy upon request by the policyholder.

For Network Dental and Vision Members:

This grace period also provides an extension of filing deadlines for claims; relaxation of prior authorization, precertification, and referral requirements; access to appropriate out-of-network providers due to unavailability on in-network providers or the members’ displacement; and leniency for any other action required under the certificate. A replacement copy of the certificate will be provided upon request by the certificate holder. Affected members should contact Aflac Benefit Solutions (formerly Argus Dental and Vision) at 855-819-1873, Option 1, for assistance.

We care about Aflac’s policyholders affected by the recent flooding:

To help provide relief for Texas policyholders and/or certificate holders residing in Bandera, Bexar, Burnet, Caldwell, Coke, Comal, Concho, Gillespie, Guadalupe, Kendall, Kerr, Kimble, Llano, Mason, McCulloch, Menard, Reeves, San Saba, Tom Green, Travis, and Williamson counties who were affected by the flooding, Aflac will provide an extended premium grace period starting July 2, 2025, and ending Sept. 8, 2025. This grace period also includes an extension of filing deadlines for claims and leniency for any other actions required under the policy and/or certificate. Aflac will provide a replacement copy of the policy and/or certificate upon request by the policyholder and/or certificate holder.

For Network Dental and Vision Members:

This grace period also includes an extension of filing deadlines for claims; temporary relaxation of prior authorization, precertification, and referral requirements; access to appropriate out-of-network providers due to unavailability of in-network providers or member displacement; and leniency for any other actions required under the certificate.

Affected members should contact Aflac Benefits Solutions (formerly Argus Dental and Vision) at 855-819-1873, option 1, for assistance.

We care about Aflac’s policyholders affected by the recent wildfires:

To help provide relief for Oregon policyholders residing in Klamath County who were affected by the wildfires, Aflac will provide a premium grace period starting July 8, 2025, and ending Sept. 08, 2025. This grace period also provides an extension of filing deadlines for claims and leniency for any other action required under the policy. Aflac will provide a replacement copy of the policy upon request by the policyholder.

For Network Dental and Vision Members:

This grace period also provides an extension of filing deadlines for claims; relaxation of prior authorization, precertification, and referral requirements; access to appropriate out-of-network providers due to unavailability on in-network providers or the members’ displacement; and leniency for any other action required under the certificate. A replacement copy of the certificate will be provided upon request by the certificate holder. Affected members should contact Aflac Benefit Solutions (formerly Argus Dental and Vision) at 855-819-1873, Option 1, for assistance.

We care about Aflac’s policyholders affected by the recent wildfires:

To help provide relief for Oregon policyholders residing in Umatilla County who were affected by the wildfires, Aflac will provide a premium grace period starting July 2, 2025, and ending Sept. 02, 2025. This grace period also provides an extension of filing deadlines for claims and leniency for any other action required under the policy. Aflac will provide a replacement copy of the policy upon request by the policyholder.

For Network Dental and Vision Members:

This grace period also provides an extension of filing deadlines for claims; relaxation of prior authorization, precertification, and referral requirements; access to appropriate out-of-network providers due to unavailability on in-network providers or the members’ displacement; and leniency for any other action required under the certificate. A replacement copy of the certificate will be provided upon request by the certificate holder. Affected members should contact Aflac Benefit Solutions (formerly Argus Dental and Vision) at 855-819-1873, Option 1, for assistance.

We care about Aflac’s policyholders affected by the recent wildfires:

To provide relief for New Mexico policyholiders and/or certificate holders residing in Grant County and affected by the Trout Fire, Aflac will provide the following protections for policyholders and/or certificate holders: Provide an extended premium grace period from Thursday, Jun. 12, 2025 through Monday, Sep. 15, 2025. Offer policyholders and/or certificate holders a payment plan of no less than six (6) months if unable to pay the delinquency after the extended day grace period (This applies to all coverages except life.). Work with policyholders and/or certificate holders on premium payments to prevent lapse and cancellation of policies. Waive late fees and penalties. Waive early refill time limits on active prescriptions. Allow additional time for actions required under the policy and/or certificate and the submission of documents due to limited access to service and mobility. Provide an extension of filing deadlines for claims and leniency for any other action required under the policy and/or certificate. Provide a copy of the policy and/or certificate to the policyholder and/or certificate holder upon request.

In addition to the above, Aflac through Aflac Benefits Solutions will provide the following protections for Network Dental and Vision members and providers: Waive cost sharing and deductibles. Permit one eyeglass or contact lens replacement and one hearing aid replacement during the pendency of the Emergency Order, waiving frequency limitations. Permit one replacement for dentures or other prosthodontic devices during the pendency of this Emergency Order, waiving frequency limits. Waive additional fees, charges, referrals, eligibility and prior authorization requirements for medically necessary services, whether emergent or not. This applies to benefits and services obtained from both in- and out-of-network providers. Extend medical providers' reporting requirements for claims submissions and for additional information relating to claims. Fully reimburse out-of-network providers at the usual, customary, and reasonable rate.

Affected members should contact Aflac Dental and Vision (formerly Argus Dental and Vision) at 855-819-1873, option 1, for assistance.

We care about Aflac’s policyholders affected by the recent weather:

To help provide relief for California policyholders residing in Trinity County affected by the Dec. 15, 2024, and Dec. 29, 2024, winter storms, Aflac will provide billing leniency for impacted insureds, an extension of filing deadlines for claims and leniency for any other action required under the policy. Aflac will provide a replacement copy of the policy upon request by the policyholder. Affected members should contact Aflac at 800-992-3522 for assistance.

For Network Dental and Vision Members:

This also provides an extension of filing deadlines for claims and leniency for any other action required under the certificate. Affected members are not required to obtain prior approval when accessing appropriate out-of-network providers when in-network providers are unavailable. The cost-sharing for out-of-network will be in amount equal to cost-sharing affected members would have paid for the provision of that service in-network. A replacement copy of the certificate will be provided upon request by the certificate holder. Affected members should contact Aflac Benefit Solutions (formerly Argus Dental and Vision) at 855-819-1873, Option 1, for assistance.

We care about Aflac’s policyholders affected by the recent levee failure:

To help provide relief for California policyholders residing in San Joaquin County affected by the Oct. 21, 2024, Victoria Island Levee failure, Aflac will provide billing leniency for impacted insureds, an extension of filing deadlines for claims and leniency for any other action required under the policy. Aflac will provide a replacement copy of the policy upon request by the policyholder. Affected members should contact Aflac at 800-992-3522 for assistance.

For Network Dental and Vision Members:

This also provides an extension of filing deadlines for claims and leniency for any other action required under the certificate. Affected members are not required to obtain prior approval when accessing appropriate out-of-network providers when in-network providers are unavailable. The cost-sharing for out-of-network will be in amount equal to cost-sharing affected members would have paid for the provision of that service in-network. A replacement copy of the certificate will be provided upon request by the certificate holder. Affected members should contact Aflac Benefit Solutions (formerly Argus Dental and Vision) at 855-819-1873, Option 1, for assistance.

We care about Aflac’s policyholders affected by the recent wildfires:

To help provide relief for California policyholders residing in Los Angeles and Ventura Counties affected by the wildfires, Aflac will provide billing leniency for impacted insureds, an extension of filing deadlines for claims and leniency for any other action required under the policy. Aflac will provide a replacement copy of the policy upon request by the policyholder. Affected members should contact Aflac at 800-992-3522 for assistance.

For Network Dental and Vision Members:

This also provides an extension of filing deadlines for claims and leniency for any other action required under the certificate. Affected members are not required to obtain prior approval when accessing appropriate out-of-network providers when in-network providers are unavailable. The cost-sharing for out-of-network will be in amount equal to cost-sharing affected members would have paid for the provision of that service in-network. A replacement copy of the certificate will be provided upon request by the certificate holder. Affected members should contact Aflac Benefit Solutions (formerly Argus Dental and Vision) at 855-819-1873, Option 1, for assistance.

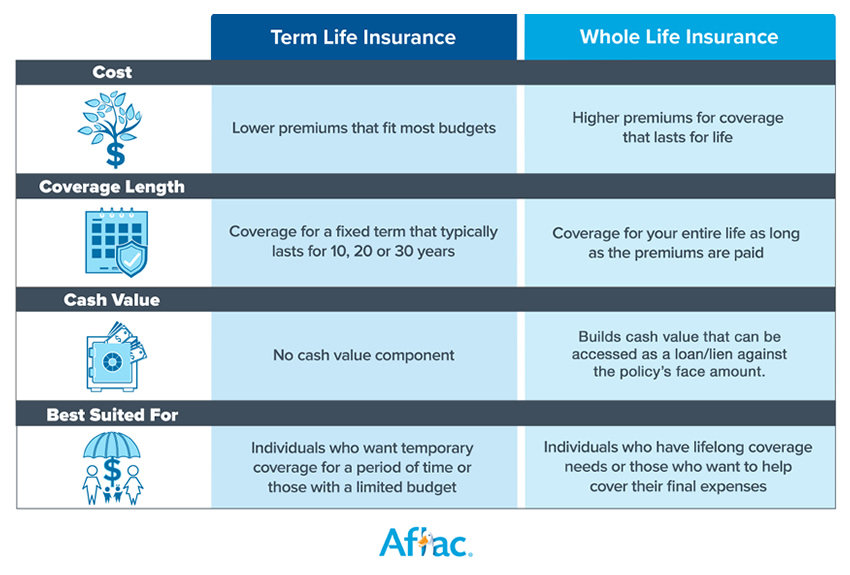

Choosing the right life insurance policy is important. Understanding the difference between term and whole life insurance is a valuable part of the decision. At Aflac, we offer a variety of life insurance plans to help meet your specific needs.

According to LIMRA, 51% of Americans reported owning some type of life insurance in January 2024. This included individual life insurance, employer-sponsored coverage, etc.1 Picking the right life insurance policy can greatly impact your retirement plan and your family’s financial security.

Table of Contents

When deciding between term or whole life insurance, there are crucial differences to take note of. Like it sounds, term life insurance provides coverage for a set term or specific amount of time. They usually vary between 10 and 30 years long. If the policyholder passes away during that specified period, your beneficiary will receive the payout.

The cost of whole life insurance vs. term varies, but term life insurance usually costs less. It costs less because there is only a payout if the timing aligns. We hope that you outlive your term, but if not, the payout can help provide support for your loved ones.

You are also able to choose your term based on your unique situation, possibly reducing costs in the long run. This choice is popular for young families because of the lower premiums upfront. It can also be a good choice for seniors factoring in their long-term plans.

When wondering, “should I buy term life insurance or whole life?” there are a few key takeaways. Whole life insurance provides coverage for your entire life cycle. Typically, whole life insurance costs more because it serves as an investment. This investment, otherwise known as the cash value, is able to grow throughout your lifetime tax-free.

When deciding between term or whole life insurance, you should note the following about whole life insurance. The premiums will not change throughout the course of your life and the death benefit is certain. You do not need to choose a term length. Lastly, the cash value will grow in a tax-deferred account at a secured rate. This is a popular choice for those looking to maximize their financial potential.

There are a few crucial differences in term and whole life insurance. We want to make it easy for you by breaking those differences down into pros and cons.

Choosing between whole life and term life insurance depends on your financial goals. We encourage you to determine what kind of financial security you’d like in place throughout your lifetime. This will allow you to assess the costs and the long-term value of term and whole life insurance accurately.

One of the main differences between whole and term life insurance is the cost. The costs of either plan vary depending on age group, gender, and medical history. Even so, whole life insurance tends to have higher premiums than term life insurance. The premiums are higher because the payments are put into an account that accumulates over time. This can provide you more security when the time comes.

Term life insurance usually has lower premiums. If you choose a 30-year term at a lower rate and your timeline is correct, your family can still receive ample security and possibly avoid higher premiums.

By now, you’ve read our analysis of whole life versus term life insurance. One isn’t necessarily better than the other, but one can be more suited for your unique needs.

We encourage to take a closer look at the costs and decide how much you are willing to spend on a policy. Considering your dependents and who you aim to support is also a key component. Lastly, you should make sure that there isn’t a better option out there for your investment purposes.

Your permanent life insurance options don’t end here. There are additional alternatives outside of whole and term life insurance.

Universal Life insurance is a great option if you want part of your policy to function as a savings account. Variable Life insurance uses sub-accounts that function similarly to mutual funds. Lastly, Indexed Universal Life Insurance allows you to adjust your premiums to maximize your cash policy’s cash value.

These options are generally only suited for specific financial goals. Most people choose between a term or whole life insurance policy. Aflac can work with you to recommend a plan that best meets your needs.

Don’t wait until it’s too late. Help cover yourself and your family with coverage from Aflac.

Get StartedIf term and whole life insurance aren’t for you, here are some alternative policies to consider:

When deciding whether to get term of whole life insurance, it’s important to consider several factors:

Ultimately, the type of policy you choose should depend on your individual needs and financial circumstances. Consider discussing all your options with a qualified professional who can help you find the right kind of policy for you.

Get Started

Looking into getting a term life insurance policy? Find out what term life insurance is and its features, rates, and benefits.

Looking into getting a whole life insurance plan? Find out how whole life insurance works and the benefits, costs, pros, and cons.

Looking into getting a term life insurance policy? Find out what term life insurance is and its features, rates, and benefits.

Looking into getting a whole life insurance plan? Find out how whole life insurance works and the benefits, costs, pros, and cons.

1 LIMRA - 2023 Life Insurance Fact Sheet. Accessed March 11, 2025. https://www.limra.com/siteassets/newsroom/liam/2024/2024-life-insurance-fact-sheet.pdf.

Content within this article is provided for general informational purposes and is not provided as tax, legal, health, or financial advice for any person or for any specific situation. Employers, employees, and other individuals should contact their own advisers about their situations. For complete details, including availability and costs of Aflac insurance, please contact your local Aflac agent.

Coverage is underwritten by American Family Life Assurance Company of Columbus. In New York, coverage is underwritten by American Family Life Assurance Company of New York.

68000 series: In Arkansas, Idaho, Oklahoma & Virginia, ICC1368100, ICC1368200, ICC1368300, ICC1368400. In Delaware, Policies A68100-A68400. B1000: In Arkansas, Idaho, Oklahoma & Virginia, Policies: ICC18B61JWO & ICC18B61JTO. In Delaware, Policies B61JWO, B61JTO. B60000: In Arkansas, Oklahoma, & Virginia, Policies: ICC18B60C10, ICC18B60100, ICC18B60200, ICC18B60300, & ICC18B60400. Q60000: Whole: In Arkansas, Delaware Policy Q60100M. In Idaho Policy Q60100MID. In Oklahoma, Policy Q60100MOK. Term: In Delaware, Policies Q60200M. In Arkansas, Idaho & Oklahoma Policies ICC18Q60200M.

Aflac Final Expense insurance coverage is underwritten by Tier One Insurance Company, a subsidiary of Aflac Incorporated and is administered by Aetna Life Insurance Company. Tier One Insurance Company is part of the Aflac family of insurers. In California, Tier One Insurance Company does business as Tier One Life Insurance Company (Tier One NAIC 92908). Not available in New York.

In Arkansas, Delaware, Idaho, Oklahoma & Virginia, Policies ICC21-AFLLBL21 and ICC21-AFLRPL21; and Riders ICC21-AFLABR22, ICC21-AFLADB22, and ICC21-AFLCDR22.

Content within this article is provided for general informational purposes and is not provided as tax, legal, health, or financial advice for any person or for any specific situation. Employers, employees, and other individuals should contact their own advisers about their situations. For complete details, including availability and costs of Aflac insurance, please contact your local Aflac agent.

Coverage may not be available in all states, including but not limited to DE, ID, NJ, NM, NY, VA or VT. Benefits/premium rates may vary based on state and plan levels. Optional riders may be available at an additional cost. Policies and riders may also contain a waiting period. Refer to the exact policy and rider forms for benefit details, definitions, limitations and exclusions.

Receipt of accelerated death benefits may affect eligibility for public assistance programs. Benefits may also be taxable and are not expected to receive the same favorable tax treatment as other types of accelerated death benefits that may be available.

Aflac | Tier One | WWHQ | 1932 Wynnton Road | Columbus, GA 31999

Aflac New York | 22 Corporate Woods Boulevard, Suite 2 | Albany, NY 12211

Z2200994R2

EXP 3/26